Tax Collection Pre and Post GST Era:

- The aggregate state and central taxes exhibited a CAGR of 11.53 per cent in the pre-GST period (FY13 to FY17) while the nominal GDP grew at a CAGR of 11.54 per cent during this period.

- CAGR of the aggregate state and central taxes was marginally less than the growth of GDP, the Tax Buoyancy was just below one .

- The Post-GST period experienced the shock of the Covid pandemic. During this period,the nominal GDP grew at a slower CAGR of 9.6 % (FY19 to FY23) while GST collections grew at a CAGR of 10.9 per cent, implying Tax Buoyancy of around 1.1.

- Improved tax collection efficiency has resulted in increased Tax Buoyancy and it is the main arguments in favor of GST.

Speaking at the GST Day 2023, The Finance Minister stated that Tax Buoyancy of states has improved to 1.22 post-GST rollout from 0.72 in the pre-GST period.

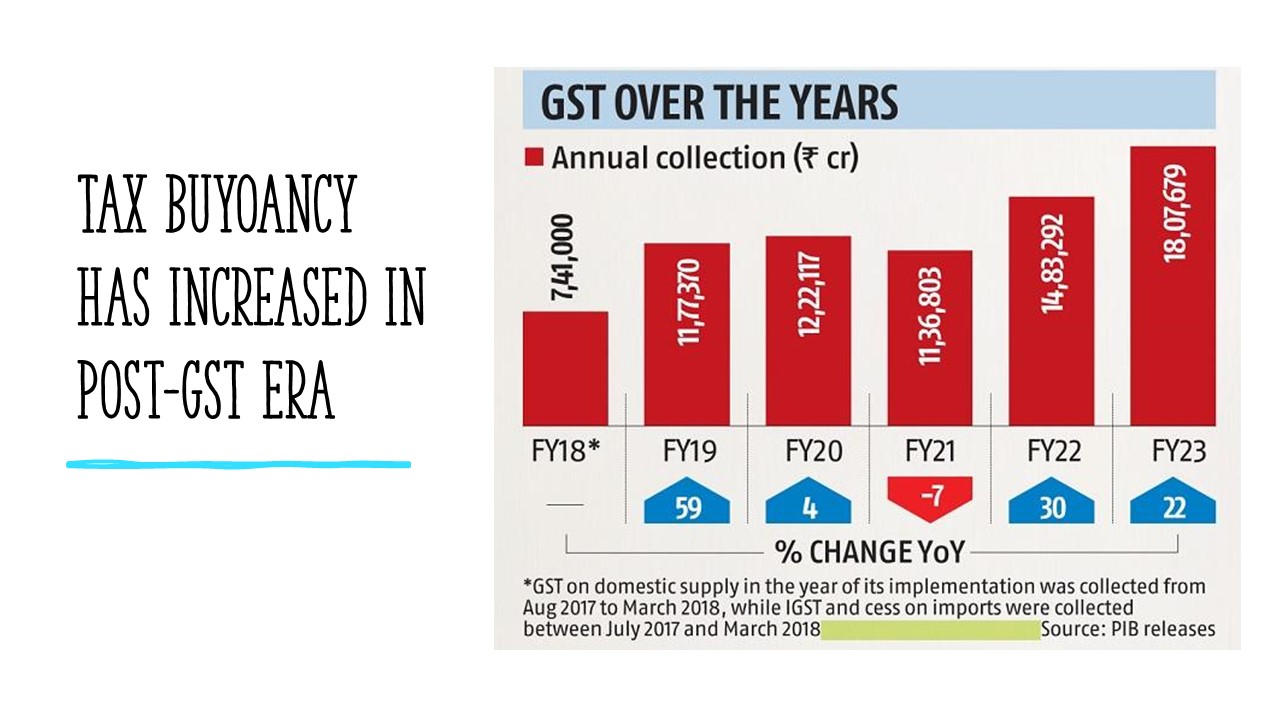

FY 2018-19---11.77 Lac Crores

FY 2019-20---12.22 Lac Crores

FY 2020-21---11.36 Lac Crores

FY 2021-22---14.76 Lac Crores

FY 2022-23---18 Lac Crores

FY 2023-24 ---20.18 Lac Crores

In the first year of GST implementation Collection was less than 1 lac crore per month while it has reached to approx. 1.7 Lac Crore in FY 24.

Challenges Of GST:

- Manufacturing states lose revenue on a bigger scale as GST is destination-based taxation .

- Input Tax Credit has certain limitations as conditions for availing ITC are stringent, leading many taxpayers to lose out on ITC.

- Taxpayers also lose their Input Tax Credit (ITC) due to non-reporting or mistakes by their suppliers.

- Wrongful or fake Input Tax Credit (ITC) claims has emerged as a major cause of concern for GST authorities.

- GST regime has the complex four tier Tax structure as ranging from 0%,5%,12%,18% and 28% along with lesser used GST Rates (.25 % and 3 %) apart from GST Compensation Cess .

- The GST regime has increased the compliance burden for taxpayers, especially for small and medium-sized enterprises (SMEs).

- GST requires taxpayers to file returns every month, which is time-consuming and complicated for SMEs.

- Despite Technological advances and compliances, still there is Tax Evasion.

- Goods and Services Tax (GST) authorities are learnt to have detected evasion of around Rs 2.01 lakh crore in 2023-24 — an amount equal to almost 10% of the total GST collected during the financial year. It is found that the majority of the alleged tax evasion was in sectors such as online gaming and casinos (Rs 83,588 crore), co-insurance/re-insurance (Rs 16,305 crore) and secondment (Rs 1,064 crore).